Why $10,000 Quietly Becomes $57,000

Leave $10,000 in an account earning 6% a year and do absolutely nothing for 30 years. Under simple interest, where you only ever earn on your original deposit, you would end with $28,000. Under compound interest, where each year's gain itself starts earning, you would end with $57,434.91 — more than double the simple-interest result, from the exact same deposit and the exact same rate.

That gap is the whole story of personal finance. It is why a 25-year-old who saves a little beats a 40-year-old who saves a lot, why credit-card balances spiral, and why Einstein supposedly called compounding the eighth wonder of the world (he probably never said it, but the math doesn't need the endorsement).

This guide explains exactly how compound interest works, with the real formula written in plain language and fully worked dollar examples you can check on a calculator. You will learn how to handle monthly contributions, why compounding frequency matters far less than most people assume, how the Rule of 72 lets you estimate doubling time in your head, and the common mistakes that quietly cost savers and borrowers real money. By the end you will be able to answer, with numbers, the question everyone actually wants answered: how much will my money grow?

Simple vs Compound Interest: The Core Difference

Simple interest is calculated only on the principal — the original amount. The formula is principal times rate times time: P x r x t. Deposit $10,000 at 6% simple interest and you earn a flat $600 every single year, forever. After 30 years that is $18,000 of interest, for a total of $28,000.

Compound interest is calculated on the principal plus all previously earned interest. Year one you earn $600 on $10,000. Year two you earn 6% on $10,600, which is $636. Year three you earn 6% on $11,236, and so on. Each year's interest is slightly larger than the last because the base it sits on keeps growing. That snowball is why the 30-year compound total reaches $57,434.91 instead of $28,000.

The difference is small at first and enormous later. After one year, simple and compound interest produce almost the same number. The two curves only fan apart over time, which is the single most important and most under-appreciated fact about money: the benefit of compounding is overwhelmingly a function of how long you stay invested, not how clever you are.

The Compound Interest Formula in Plain English

The standard future-value formula looks intimidating but reads simply once you name the parts. It is: A equals P times the quantity one plus r divided by n, all raised to the power of n times t.

Written as an equation: A = P x (1 + r/n)^(n x t).

Here is what each letter means. A is the final amount you end up with. P is the principal, your starting deposit. r is the annual interest rate written as a decimal, so 6% is 0.06. n is the number of times interest is compounded per year — 1 for annual, 12 for monthly, 365 for daily. And t is the number of years.

The logic: r divided by n is the interest rate for one short period (the monthly rate, say). One plus that rate is your growth multiplier for a single period. Raising it to the power of n times t applies that growth once for every period across the whole timeframe. Multiply by your starting principal and you have the ending balance.

A fully worked example. You deposit $10,000 (P = 10000) at 7% annual interest (r = 0.07), compounded monthly (n = 12), for 10 years (t = 10). The monthly rate is 0.07 / 12 = 0.0058333. The number of periods is 12 x 10 = 120. So A = 10000 x (1.0058333)^120 = $20,096.61. Your money has roughly doubled, and the interest earned is $20,096.61 minus the $10,000 principal, which is $10,096.61.

To isolate just the interest rather than the total, subtract the principal at the end: total interest equals A minus P. Nothing more complicated than that.

Adding Monthly Contributions: The Realistic Scenario

Almost nobody deposits one lump sum and walks away. Real saving means adding money every month — to a 401(k), an ISA, an RRSP, or a brokerage account. That requires a second formula on top of the first, because each contribution compounds for a different length of time. The dollar you add today compounds for the full term; the dollar you add in the final month barely compounds at all.

The future value of a stream of equal contributions is: PMT times the quantity one plus i raised to the power N, minus one, all divided by i. Written out: contribution future value = PMT x (((1 + i)^N - 1) / i).

In that formula, PMT is the amount you contribute each period, i is the periodic interest rate (the annual rate divided by how many times per year you contribute), and N is the total number of contributions (contributions per year times the number of years). This version assumes contributions are made at the end of each period. One edge case worth knowing: if the rate i is zero, the formula breaks down mathematically, and the future value is simply PMT times N — you just get back everything you put in.

A worked example combining both pieces. You start with $5,000 (P), add $300 at the end of every month (PMT), earn 8% annually compounded monthly (so i = 0.08 / 12 = 0.0066667), for 20 years (N = 12 x 20 = 240 periods).

The starting $5,000 grows on its own to 5000 x (1.0066667)^240 = $24,634.01.

The stream of $300 contributions grows to 300 x (((1.0066667)^240 - 1) / 0.0066667) = $176,706.12.

Add them together and the ending balance is $201,340.14. Over those 20 years you personally contributed $5,000 plus 240 payments of $300, which is $72,000, for $77,000 of your own money in total. The remaining $124,340.14 is pure compound interest. You roughly tripled your contributions without doing anything except staying invested. Running this exact scenario in a Compound Interest Calculator takes seconds and lets you slide the contribution and the rate to see how the final number reacts.

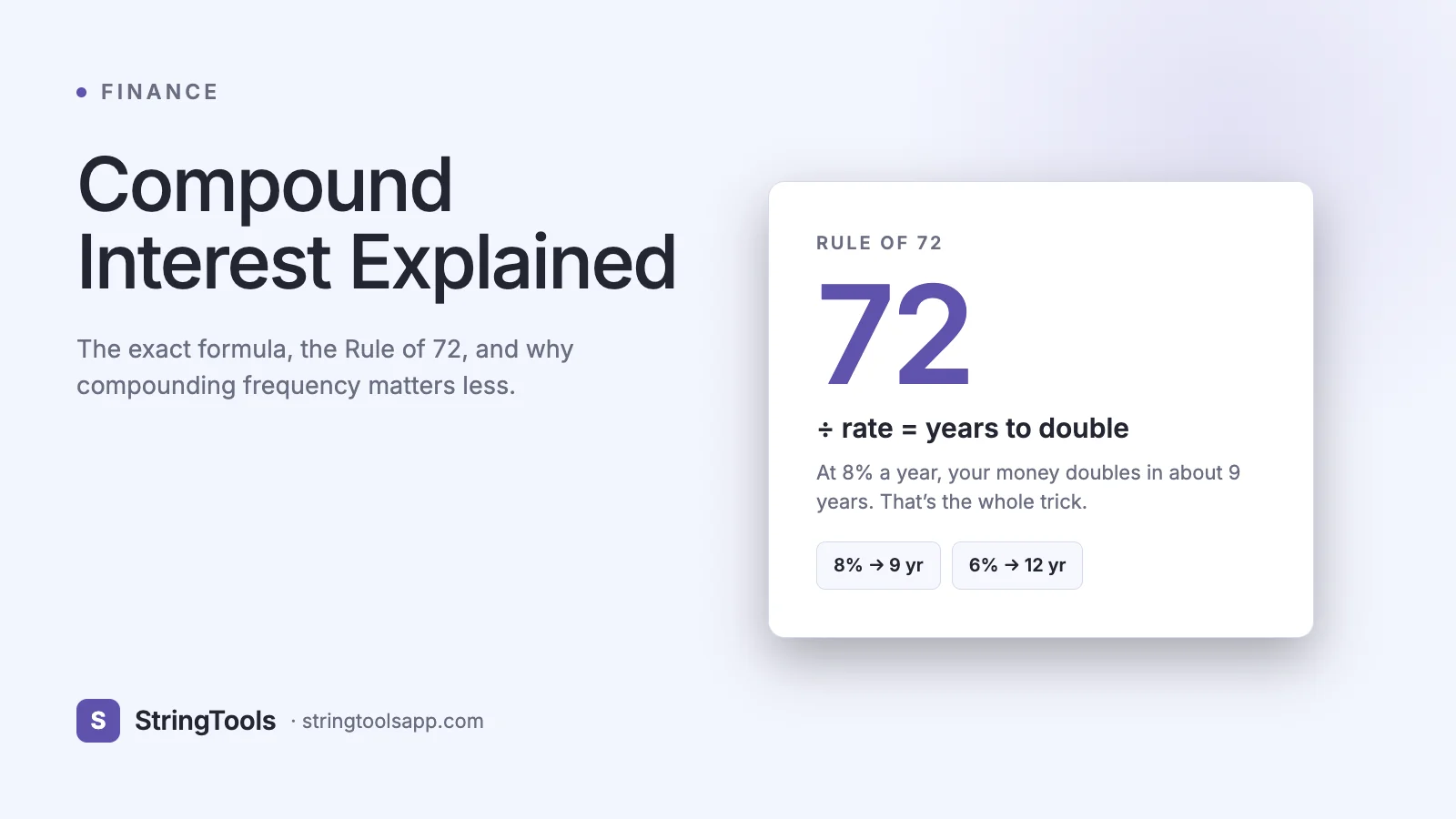

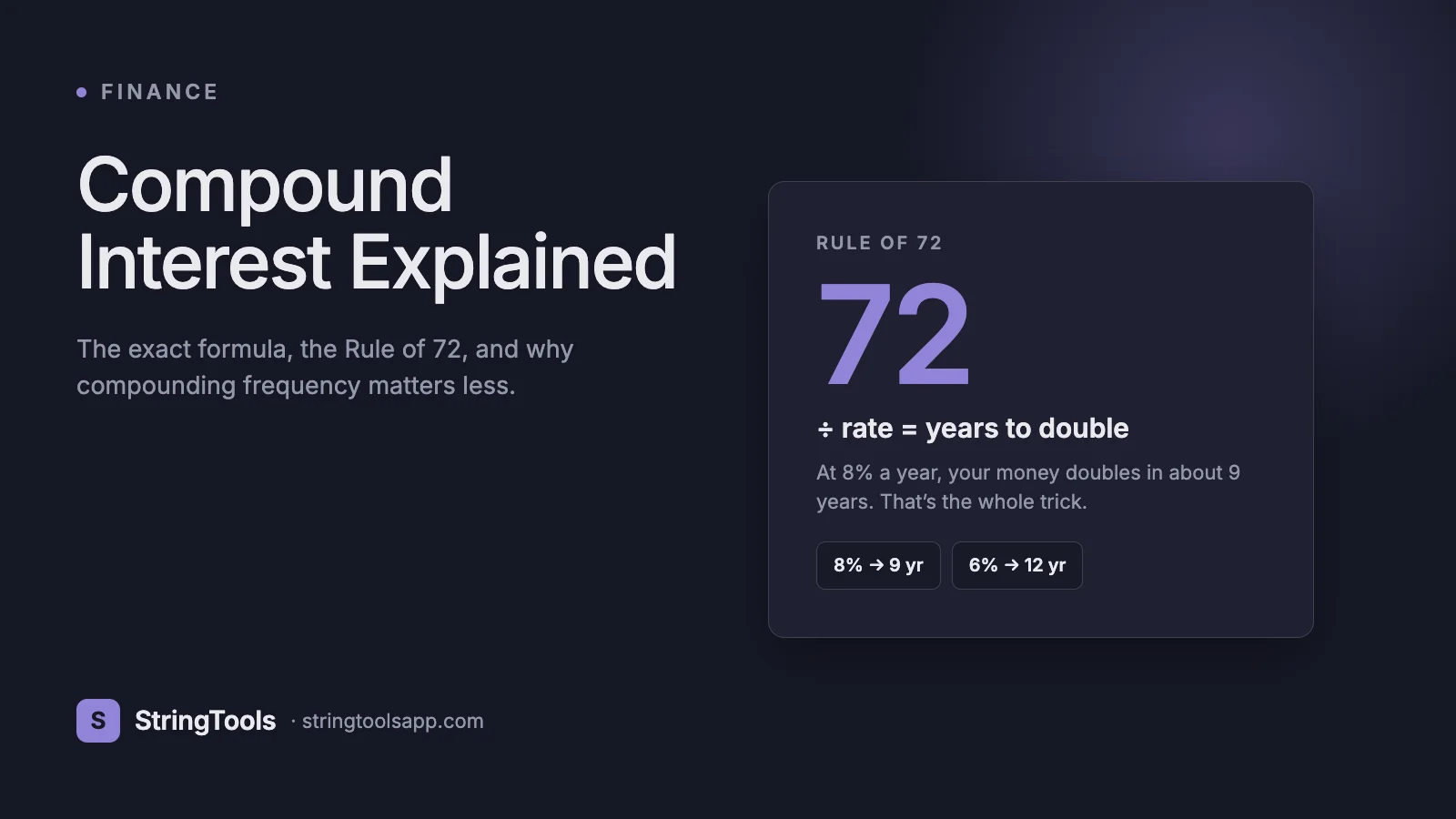

The Rule of 72: Doubling Time in Your Head

The Rule of 72 is the most useful piece of financial mental math ever invented. To estimate how many years it takes for your money to double, divide 72 by the annual interest rate written as a whole number.

At 6%, money doubles in about 72 / 6 = 12 years. At 8%, about 72 / 8 = 9 years. At 9%, about 8 years. At 12%, about 6 years. The rule works in reverse too: if you need your money to double in 10 years, you need roughly 72 / 10 = 7.2% annual return.

How accurate is it? Remarkably so for the rates ordinary savers and investors deal with. The true doubling time at 6% is 11.9 years versus the rule's 12. At 8% the true figure is 9.01 versus 9. At 9% it is 8.04 versus 8. The approximation is tightest in the 6% to 10% band and drifts a little at very high rates, but for back-of-envelope planning it is excellent.

The Rule of 72 also makes the cost of debt visceral. A credit card at 24% APR doubles a balance you never pay down in about 72 / 24 = 3 years. The same mathematics that builds wealth on the saving side destroys it on the borrowing side, just pointed in the opposite direction.

Does Compounding Frequency Actually Matter?

Banks love to advertise daily compounding as if it were a meaningful advantage. The honest answer is that it barely matters. Take $10,000 at 6% for one year and watch what changes as you compound more often.

Compounded annually, you end with $10,600.00. Compounded semi-annually (twice a year), $10,609.00. Quarterly, $10,613.64. Monthly, $10,616.78. Daily, $10,618.31.

Going from once a year to every single day adds a grand total of $18.31 on a $10,000 balance. The reason is that there is a mathematical ceiling: as compounding frequency approaches infinity, the result converges on continuous compounding, and the gap between monthly and continuous is trivial. The first jump, from annual to monthly, captures almost all of the available benefit; everything past monthly is rounding error.

The practical takeaway is to ignore frequency marketing and focus on the two variables that genuinely move the needle: the annual rate and the number of years. A half-percent better rate or five more years invested will dwarf any difference between daily and monthly compounding. This is also why you should always compare accounts using APY (annual percentage yield) rather than the nominal rate — APY bakes the compounding frequency into a single honest number you can compare apples to apples.

Common Mistakes and Misconceptions

Mistake one: confusing nominal rate with APY. A 6% rate compounded monthly is not the same as 6% earned. Its effective annual yield is about 6.17%. When comparing a savings account to a bond or a CD, always compare the effective annual yield, never the headline number.

Mistake two: starting late and trying to catch up with bigger contributions. Because compounding rewards time exponentially, the early years are worth far more than the late ones. Contributing $200 a month at 6% for 40 years produces $398,298.15. Waiting ten years and contributing the same $200 a month for 30 years produces only $200,903.01 — roughly half, for putting in only $24,000 less. The missing decade, not the missing dollars, did the damage.

Mistake three: forgetting that inflation compounds too. A nominal 7% return with 3% inflation is closer to a 4% real return. Your money grows, but its purchasing power grows more slowly. For long-range planning, run the numbers a second time using an inflation-adjusted real rate.

Mistake four: assuming a steady rate is reality. Real investment returns are volatile; the formula gives you a clean projection, not a guarantee. A 7% average can include years of minus 20% and plus 25%. Use compound projections to set expectations and direction, not as a promise.

Mistake five: ignoring fees and taxes, which compound against you exactly the way returns compound for you. A 1% annual fund fee does not cost you 1% — over decades it can quietly consume a fifth or more of your final balance, because every dollar skimmed is a dollar that never compounds again.

Quick Answers to Common Questions

What is compound interest, in one sentence? It is interest calculated on both your original money and on the interest that money has already earned, so your balance grows at an accelerating rate over time.

What is the difference between compound and simple interest? Simple interest is earned only on the original principal and grows in a straight line; compound interest is earned on the principal plus accumulated interest and grows on a curve that steepens over time. Over short periods they are nearly identical; over decades compound interest wins enormously.

How do I calculate compound interest? Use A = P x (1 + r/n)^(n x t), where P is your starting amount, r is the annual rate as a decimal, n is how many times per year it compounds, and t is the number of years. Subtract P from A to find the interest alone.

What is the Rule of 72 and is it accurate? Divide 72 by the interest rate as a whole number to estimate years to double. At 8% that is 9 years, and the true value is 9.01 — so yes, it is highly accurate for everyday rates between roughly 4% and 12%.

How much will my money grow with regular contributions? Add the lump-sum growth of your starting balance to the future value of your contribution stream, PMT x (((1 + i)^N - 1) / i). For example, GBP 500 a month at 5% for 25 years grows to about GBP 297,754.85, of which only GBP 150,000 is money you contributed.

Run Your Own Numbers

Compound interest is not a personality trait or a stroke of luck — it is arithmetic, and now you have the formula, the contribution math, and the Rule of 72 to reason about it. The two levers that matter most are obvious once you have seen the curves: the annual rate you can realistically earn, and the number of years you stay invested. Time, not timing, is what builds the balance.

The fastest way to internalize all of this is to put your own figures in and watch the total move. Open our Compound Interest Calculator at https://stringtoolsapp.com/compound-interest-calculator, enter your starting amount, your monthly contribution, a sensible rate, and a time horizon, and it will return your future value, your total contributions, and the interest earned — instantly, with the exact formulas from this article doing the work behind the scenes. Try nudging the time horizon up by five years, or the rate up by half a percent, and notice how much the ending number jumps; that sensitivity is the power of compounding made visible.

If you are evaluating a loan rather than savings, the same compounding math runs in reverse against you — our EMI Calculator at /emi-calculator shows how interest stacks up on borrowed money, and the GST Calculator at /gst-calculator and Income Tax tools can help you plan what you actually keep.

A quick disclaimer: every figure produced by a compound interest formula is an estimate based on a constant assumed rate, and real-world returns, fees, taxes, and inflation will vary. Use these projections for planning and direction, not as guaranteed outcomes, and confirm any specific savings, investment, or loan decision with a qualified financial professional or your lender before acting on it.