Why Your First Loan Payment Barely Moves the Balance

You sign for a $300,000 mortgage at 6.5% over 30 years. Your monthly payment is about $1,896. After your very first payment clears, you check the balance expecting to see roughly $1,896 knocked off. Instead it has dropped by just $271. The other $1,625 vanished into interest. For most borrowers this is the moment loan amortization stops being an abstract word and becomes a very real, very expensive surprise.

This is not a trick by your lender. It is simply how amortizing loans work, and once you understand the mechanism you gain real power over the loan: the ability to see exactly where your money goes each month, to compare offers honestly, and to shave years and tens of thousands of dollars off the total cost with moves that take five minutes to set up.

In this guide you will learn what amortization actually is, the exact formula behind your monthly payment (explained in plain language with a fully worked example), why early payments are mostly interest, the real difference between APR and the interest rate, how shorter versus longer terms change the math, and precisely how extra payments cut both your interest and your payoff date. We will use dollar examples throughout, with notes for readers in the UK, Canada, and Australia where the mechanics are identical even if the products are named differently.

What an Amortization Schedule Actually Is

Amortization simply means spreading a debt out so it is fully paid off by a fixed end date through equal, regular payments. A mortgage, a car loan, a personal loan, and most student loans are amortizing loans. A credit card is not, which is exactly why credit card debt is so dangerous: there is no fixed payoff date built in.

An amortization schedule is the month-by-month table that shows, for every single payment over the life of the loan, three numbers: how much of that payment goes to interest, how much goes to principal (the actual debt you borrowed), and what the remaining balance is afterward.

The key idea is that your monthly payment stays the same every month, but the split between interest and principal changes constantly. Interest is always charged on the balance you still owe. At the start, you owe a lot, so the interest slice is large and the principal slice is small. As the balance shrinks, the interest slice shrinks too, so more of your fixed payment attacks the principal. This is why the schedule is sometimes described as a slow-motion seesaw: interest high and principal low at the beginning, gradually tipping until principal dominates near the end.

That single mechanic, interest charged on the remaining balance, explains almost everything else in this article.

The Formula, Explained in Plain English

Your fixed monthly payment is set by one equation that solves a simple question: what equal amount, paid every month, will exactly zero out the loan by the final payment?

The formula is M = P times r times (1 + r) to the power n, divided by ((1 + r) to the power n minus 1).

Here M is the monthly payment, P is the principal (the amount you borrow), r is the monthly interest rate, and n is the total number of monthly payments. The monthly rate r is the annual rate divided by 12 and then divided by 100 to turn a percentage into a decimal. So a 6.5% annual rate becomes 0.065 divided by 12, or about 0.005417 per month. And n for a 30-year loan is 30 times 12, which is 360 payments. (If a loan somehow charged zero interest, the formula collapses to the obvious: M equals P divided by n.)

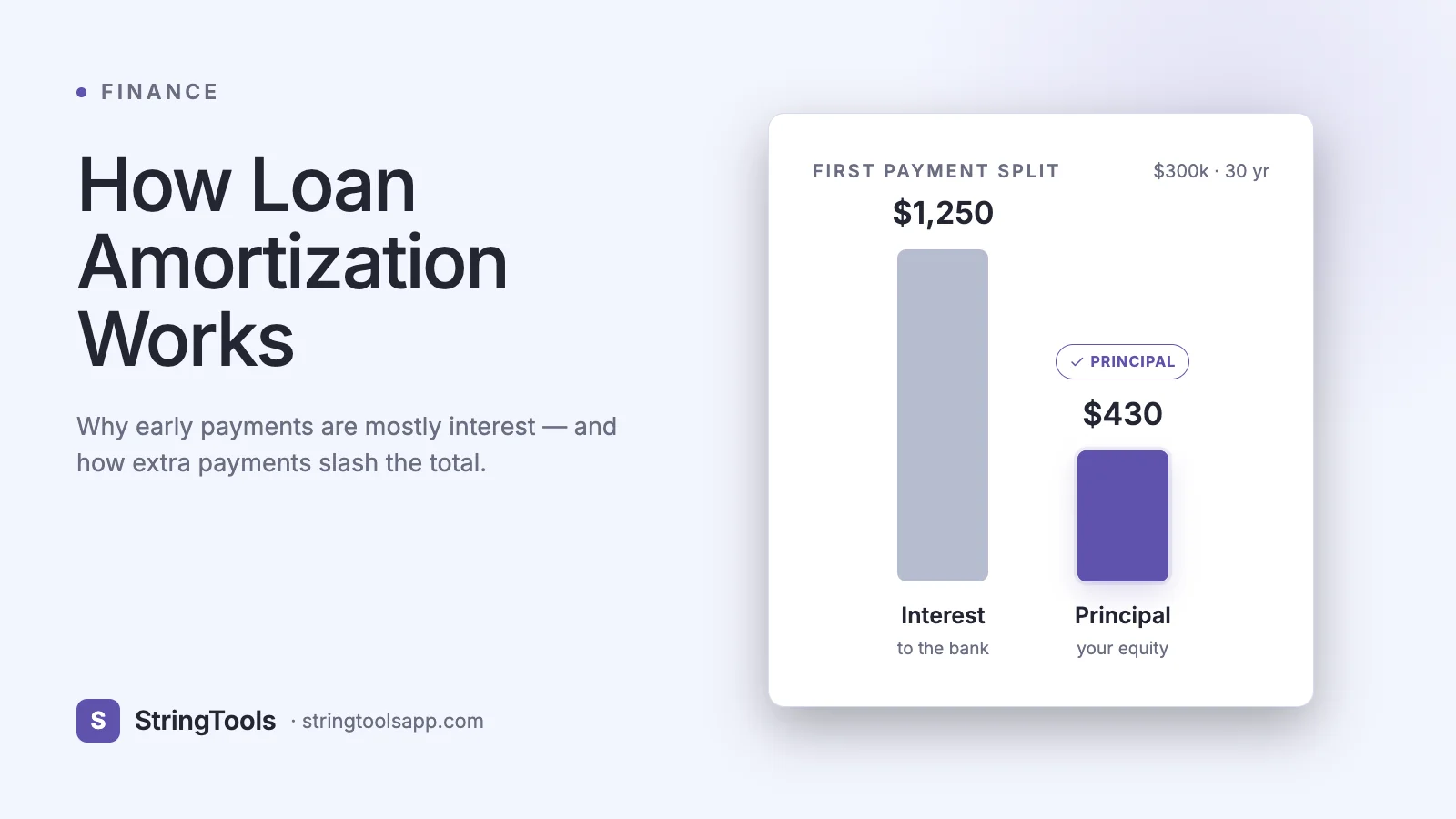

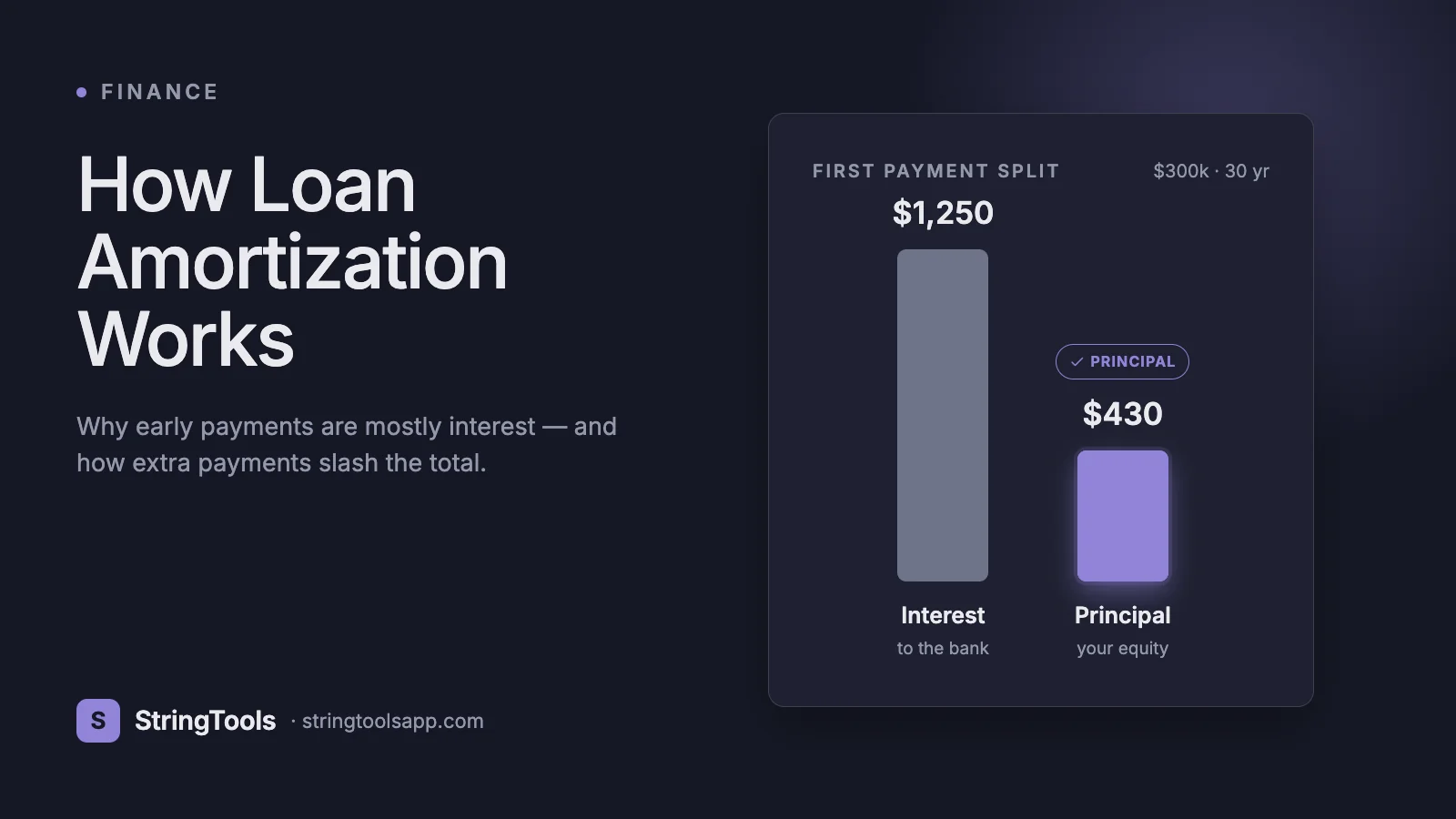

Let us work the $300,000 mortgage all the way through. P is 300,000, r is 0.005417, and n is 360. Plug those in and the monthly payment M comes out to about $1,896.20. Over all 360 payments you will hand the lender about $682,633 in total, which means roughly $382,633 of that is pure interest, more than the house price itself.

Now watch the first payment split. Interest for month one is the balance times the monthly rate: $300,000 times 0.005417, which is $1,625. Since your payment is $1,896.20, the principal portion is $1,896.20 minus $1,625, or $271.20. Your new balance is $300,000 minus $271.20, equal to $299,728.80.

Month two repeats the exact same logic on the slightly smaller balance. Interest is $299,728.80 times 0.005417, which is about $1,623.53, a tiny bit less than last month. Principal is therefore $1,896.20 minus $1,623.53, about $272.67, a tiny bit more. And so it goes, 360 times, with the interest portion creeping down and the principal portion creeping up every single month until the final payment clears the balance to zero.

Why Early Payments Are Mostly Interest

The reason early payments are so interest-heavy is not psychology or fine print. It is that interest is charged on the balance you still owe, and at the beginning you owe nearly the entire loan. With $300,000 outstanding, even a modest 6.5% rate generates $1,625 of interest in a single month. There is simply not much room left in your $1,896 payment for principal.

The crossover point, the month where your principal portion finally exceeds your interest portion, comes surprisingly late. On this 30-year loan it does not arrive until around payment 233, which is more than 19 years into the loan. For the first nineteen-plus years, the majority of every payment is feeding interest rather than building equity.

This front-loading has two important consequences. First, it is why the early years of a long mortgage build equity so slowly, and why someone who sells or refinances after a few years has barely dented the principal. Second, it is why extra payments made early are so powerful, a point we return to below. A dollar of extra principal paid in year one removes that dollar from every future interest calculation for the remaining 29 years; the same dollar paid in year 25 only saves five years of interest. Early extra dollars do the most work.

APR vs Interest Rate: The Number That Actually Compares Lenders

The interest rate, sometimes called the nominal or note rate, is the percentage used in the amortization formula to compute your interest each month. It is the number that determines your monthly payment.

The APR, or Annual Percentage Rate, is a broader figure that folds the interest rate together with most of the upfront costs of the loan: origination fees, points, certain closing costs, and similar charges, expressed as a single annualized percentage. Because it includes those fees, the APR is always equal to or higher than the plain interest rate, never lower.

That difference is exactly why APR is the better number for comparing offers across lenders. Imagine Lender A advertises 6.4% and Lender B advertises 6.5%. At a glance, A looks cheaper. But if Lender A charges $6,000 in points and fees while Lender B charges almost nothing, Lender A's APR might be 6.7% while Lender B's is 6.55%. Once fees are baked in, Lender B is the cheaper loan. Comparing only the headline interest rate would have led you to the worse deal.

UK readers will recognize this as the representative APR required on credit advertising; Canadian and Australian lenders disclose a comparison rate or APR for the same purpose. The rule is universal: use the interest rate to understand your payment, and use the APR to choose between lenders. One important caveat is that APR assumes you hold the loan for its full term, so if you expect to refinance or sell early, a low-fee, slightly-higher-rate loan can sometimes beat a low-rate, high-fee one. When in doubt, run both scenarios.

Shorter vs Longer Terms, and Auto vs Personal Loans

The loan term, the n in the formula, has a dramatic effect that surprises many borrowers. Take the same $300,000 at 6.5%. Over 30 years the payment is about $1,896 and total interest is roughly $382,633. Shorten the term to 15 years and the payment rises to about $2,613, only about 38% more per month, but total interest collapses to roughly $170,398. By choosing the shorter term you pay an extra $717 a month and save more than $212,000 in interest over the life of the loan.

The trade-off is real, though. A longer term means a smaller, more affordable monthly payment but far more total interest, because you owe money for longer and interest accrues every one of those extra months. A shorter term means a higher monthly payment but dramatically less total cost. The right choice depends on your cash flow and your other financial goals, not on which number looks smaller in isolation.

This is also where loan type matters. An auto loan is secured by the car, so rates are typically lower and terms shorter, often 36 to 72 months. For example, $25,000 at 7% over 60 months works out to about $495 a month and only about $4,702 in total interest. A personal loan is usually unsecured, meaning no collateral backs it, so lenders charge higher rates to cover their risk, and terms are often shorter still, commonly two to five years. Borrowing the same $25,000 as an unsecured personal loan would typically carry a meaningfully higher rate and therefore a higher payment and more interest, even over an identical term. The lesson: a secured loan against an asset you are buying is almost always cheaper than unsecured borrowing for the same amount.

Does Paying Extra Really Reduce Interest? Yes, and Here Is the Proof

This is the single most valuable thing to understand about amortization. Any extra amount you pay above your required monthly payment goes entirely to principal. It skips the interest line completely. And because all future interest is calculated on the remaining balance, every extra dollar of principal permanently removes its share of interest from every future month.

Return to the $300,000, 30-year, 6.5% mortgage with its $1,896 payment. Suppose you add just $200 a month, paying $2,096 instead. That extra $200 attacks principal every month from day one. The result: the loan is fully paid off in about 277 months instead of 360, roughly 23 years instead of 30. You finish about 7 years early and save approximately $103,449 in interest, all from an extra $200 a month that most households can find by trimming elsewhere.

Notice the leverage. You contributed extra principal of $200 times 277 months, about $55,400 of your own money, and it saved you over $103,000 in interest. That is because each early extra dollar dodges decades of compounding interest. The earlier in the loan you make extra payments, the larger the savings, which is the practical flip side of the front-loading we saw earlier.

A few cautions. Before sending extra money, confirm your loan has no prepayment penalty (most US mortgages do not, but some personal and auto loans do, and this is worth checking in the UK and Australia too). Also tell your servicer in writing to apply extra funds to principal, not to prepay future scheduled payments, or the benefit can be lost. Even occasional lump sums, such as a tax refund or bonus, produce the same kind of outsized savings when applied to principal early.

Quick Answers and Where to Run Your Own Numbers

How does loan amortization work? Your payment stays fixed, but each month interest is charged on the balance you still owe; whatever is left of the payment reduces the principal, which shrinks the balance and lowers next month's interest, slowly tipping the split from mostly interest toward mostly principal.

What is an amortization schedule? It is the full month-by-month table showing, for every payment, how much went to interest, how much went to principal, and the remaining balance, all the way down to zero on the final payment.

What is the difference between APR and the interest rate? The interest rate sets your monthly payment; the APR adds in fees and points to give a single comparison number that is always equal to or higher than the rate, and it is the better figure for comparing lenders.

Does paying extra actually reduce interest? Yes. Extra payments go straight to principal, which lowers the balance every future month's interest is calculated on, cutting both total interest paid and the number of months until payoff, with the biggest savings coming from extra payments made early.

Is a shorter term always better? Not always. A shorter term saves enormous interest but demands a higher monthly payment; the right answer depends on whether that payment fits your budget without crowding out savings, emergencies, and other goals.

The best way to make any of this concrete is to model your own loan. Open our free Loan Calculator at https://stringtoolsapp.com/loan-calculator, enter your principal, rate, and term, and you will instantly see your monthly payment, total interest, and a full amortization schedule. Then try adding an extra $100 or $200 a month in the Loan Calculator and watch the payoff date and total interest drop in real time. Seeing your own numbers move is far more persuasive than any general rule.

A quick disclaimer: every figure in this guide is an estimate for illustration, using simple monthly compounding and ignoring taxes, insurance, and lender-specific fees. Your actual loan terms, escrow, and total cost can differ. Before making a borrowing or prepayment decision, confirm the exact numbers with your lender and, where appropriate, a qualified financial professional.