The Number on Your Lender's Quote Is Not One Number

When a lender tells you your mortgage payment will be "about $1,900 a month," they are quoting you a blend of four or five separate things stacked on top of each other. Most first-time buyers assume the whole payment goes toward the house. In reality, in the early years the overwhelming majority of it goes to interest and escrow, and only a sliver chips away at what you actually owe.

That gap between what people think they are paying and what they are actually paying is where expensive mistakes happen. Buyers stretch to a payment they cannot sustain, get surprised when their payment jumps after year one, or carry private mortgage insurance for years longer than the law requires because nobody told them how to cancel it.

This guide takes the mystery out of it. You will learn the exact formula lenders use to calculate principal and interest, what the acronym PITI actually contains, what PMI is and the precise point at which it must legally stop, how amortization quietly front-loads your interest, the difference between a 15-year and a 30-year loan in real dollars, and how much house you can responsibly afford using the 28/36 rule. Every example uses real arithmetic you can reproduce, and we close by showing you how to run your own numbers in seconds with our Mortgage Calculator.

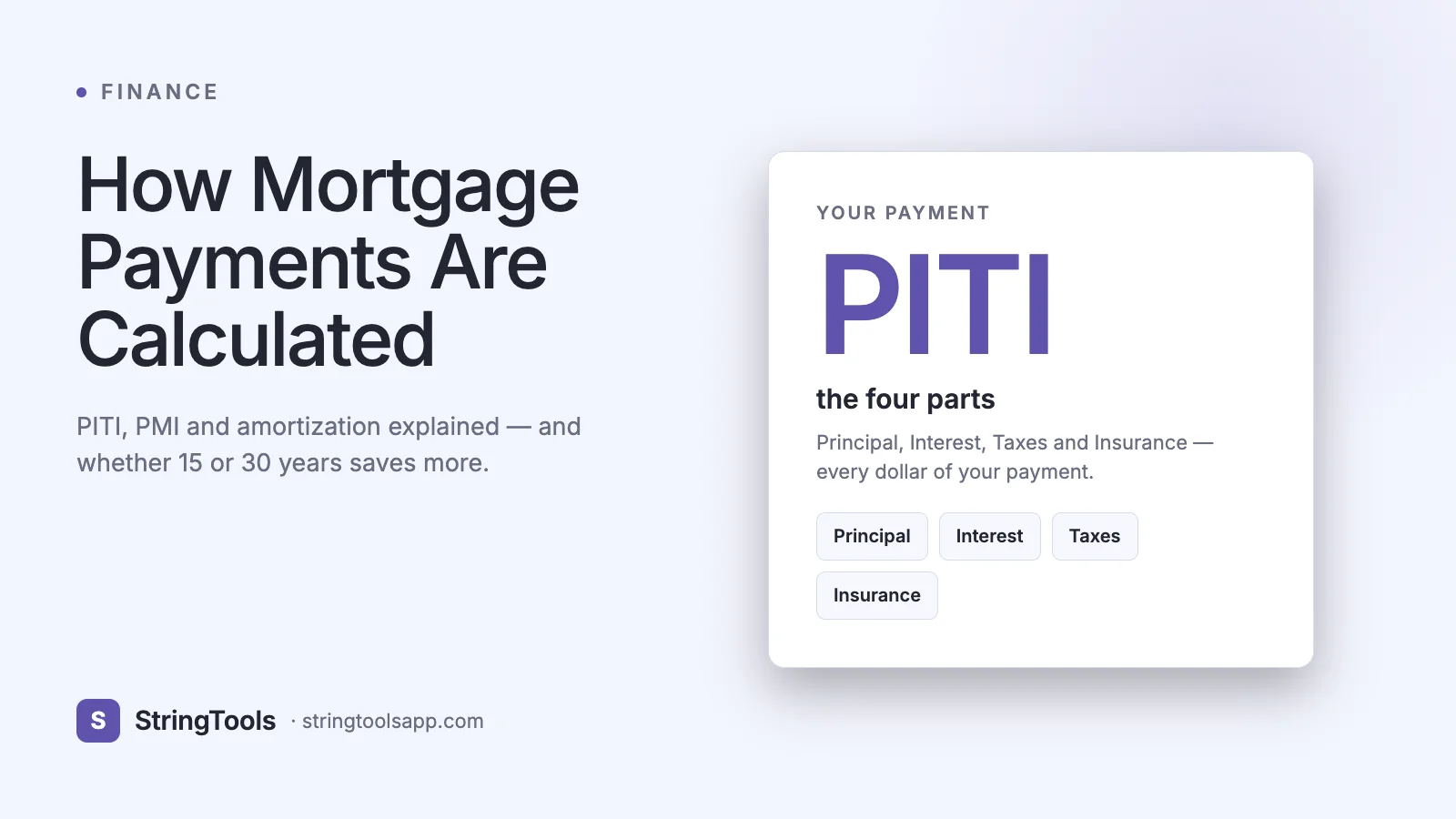

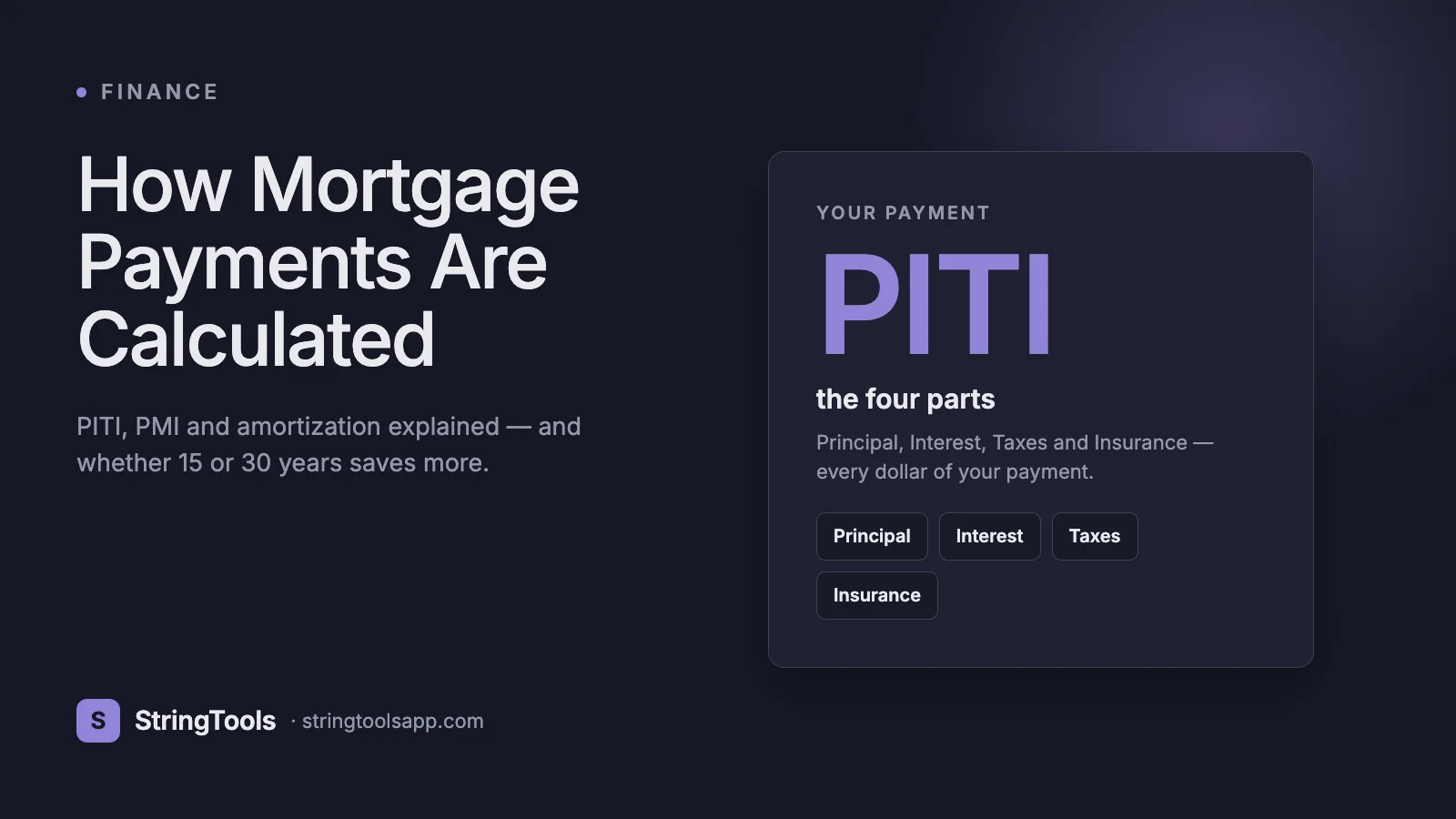

What PITI Actually Stands For

Your total monthly housing payment is usually written as PITI. It is the sum of four parts, and understanding each one is the single most useful thing you can learn before signing.

P and I — Principal and Interest. This is the loan repayment itself, the part calculated by the mortgage formula. Principal is the amount that reduces your balance; interest is the lender's charge for the money. Together they are a single fixed figure on a fixed-rate loan.

T — Taxes. Property taxes set by your county or city, collected monthly by the lender and held in an escrow account, then paid to the taxing authority once or twice a year on your behalf.

I — Insurance. Homeowners insurance, also collected monthly into escrow. Lenders require it to protect the collateral. In flood or hurricane zones this can be a meaningful line item.

People often add two more pieces beyond the strict PITI acronym. The first is PMI, private mortgage insurance, which applies when your down payment is under 20 percent. The second is HOA dues if your property sits in a homeowners association or condo building.

So the full picture is: total monthly payment equals principal and interest, plus monthly property tax, plus monthly homeowners insurance, plus monthly PMI if applicable, plus any HOA dues. This is why a $300,000 loan with a $1,896 principal-and-interest figure can easily cost $2,500 or more once everything is stacked on. When you compare quotes, always confirm whether the number you are given is just principal and interest or the full PITI, because lenders are not consistent about which one they lead with.

The Formula Behind Principal and Interest

The fixed monthly principal-and-interest payment comes from one standard formula used across the entire industry. In plain terms it is:

M equals P times r times (1 plus r) to the power n, all divided by (1 plus r) to the power n minus 1.

Here P is the loan amount, which is your home price minus your down payment. The value r is the monthly interest rate, found by taking the annual rate, dividing by 12, then dividing by 100 to turn a percentage into a decimal. And n is the total number of monthly payments, which is the loan term in years times 12. There is one special case: if the interest rate is exactly zero, the formula collapses to simply M equals P divided by n, because there is no interest to compound.

Let us walk a complete example. Suppose you borrow $300,000 at a 6.5 percent annual rate over 30 years. First, the monthly rate r is 6.5 divided by 12 divided by 100, which is about 0.0054167. The number of payments n is 30 times 12, which is 360. Plug those into the formula and the monthly principal and interest works out to about $1,896.20.

That single payment never changes on a fixed-rate loan. Over the full 360 months you would pay roughly $682,633 in total, of which about $382,633 is pure interest. In other words, on this loan you pay back more in interest than the original price of the house. That fact alone reshapes how most people think about rate, term, and extra payments, and it is the reason the next two sections matter so much.

How Amortization Front-Loads Your Interest

Amortization is the schedule that splits each fixed payment into its interest portion and its principal portion, month by month, until the balance reaches zero. The mechanics are simple but the consequences are not intuitive.

Each month, the lender first calculates interest on the current outstanding balance. Whatever is left of your payment after that interest is charged goes toward principal. Because your balance starts high, the interest slice starts large and the principal slice starts small. As the balance falls, the interest slice shrinks and the principal slice grows. The payment total stays identical, but the mix shifts steadily over time.

Return to the $300,000 loan at 6.5 percent. In the very first month, interest is the balance times the monthly rate, which is $300,000 times 0.0054167, or exactly $1,625. Since the total payment is $1,896.20, only about $271.20 goes to principal that first month. You sent the lender nearly $1,900 and your loan balance barely moved.

This front-loading is why selling or refinancing in the first few years feels like you have built almost no equity, and it is why two loans with the same payment but different interest splits behave so differently. It is also the key to understanding why extra principal payments early in the loan are so powerful, which we cover below. A full amortization schedule, available in any good Mortgage Calculator, lets you see exactly how the split evolves for your specific loan.

PMI: What It Is and Exactly When It Stops

Private mortgage insurance, or PMI, is an extra monthly charge that protects the lender, not you, in case you default. It typically applies whenever your down payment is less than 20 percent of the home's value, because a smaller down payment means the lender is carrying more risk.

PMI usually runs somewhere between about 0.3 percent and 1.5 percent of the loan amount per year, depending on your credit score and how little you put down. As an example, on a $225,000 loan, a PMI rate of 0.5 percent per year is $1,125 annually, or about $93.75 a month added on top of your PITI. That is real money for a charge that builds you no equity.

The good news is that PMI does not last forever, and US federal law is specific about this. Under the Homeowners Protection Act, you can request that your lender cancel PMI once your loan-to-value ratio reaches 80 percent, meaning you owe 80 percent of the original value. More importantly, the lender is legally required to automatically terminate PMI once your balance is scheduled to reach 78 percent of the original value, provided you are current on payments. On a $250,000 home, 78 percent is a balance of $195,000, so PMI must drop off automatically once your scheduled balance crosses that mark.

Two practical notes. First, the automatic cutoff is based on the original amortization schedule, so making extra payments does not automatically trigger it earlier, but it does let you request cancellation sooner once you cross 80 percent. Second, this framework applies to conventional loans. Government-backed FHA loans handle mortgage insurance very differently, and in many cases that insurance lasts the life of the loan unless you refinance. Always confirm which type you have.

15 vs 30 Years, and How Much House You Can Afford

The single biggest lever on your payment, after the rate, is the term. A 30-year loan spreads payments thin and keeps the monthly figure low, while a 15-year loan demands more each month but saves a fortune in interest.

Compare the same $300,000 loan at 6.5 percent. Over 30 years the principal and interest is about $1,896 a month and total interest is roughly $382,633. Over 15 years the payment rises to about $2,613 a month, but total interest collapses to about $170,398. You pay roughly $717 more each month and save more than $212,000 in interest. Real-world 15-year rates are often slightly lower too, which widens the gap further. The trade-off is straightforward: the 30-year buys you payment flexibility and breathing room, the 15-year buys you enormous long-run savings and faster equity.

That raises the question every buyer asks: how much house can I actually afford? The most widely used guideline is the 28/36 rule. It says your total housing payment, the full PITI, should not exceed 28 percent of your gross monthly income, and your total debt payments, including the mortgage plus car loans, student loans, and minimum credit card payments, should not exceed 36 percent of gross monthly income.

Here is how to apply it. Suppose you earn $90,000 a year, which is $7,500 a month gross. The 28 percent housing cap is $2,100 a month for your entire PITI. The 36 percent total-debt cap is $2,700 a month for all debt combined, so if you already pay $400 on a car loan, that leaves $2,300 for housing, and the lower of the two figures, $2,100, governs. Working backward from a $2,100 PITI, and reserving several hundred dollars of it for taxes, insurance, and PMI, tells you the loan size and price range you can responsibly target. These percentages also translate cleanly to other markets such as the UK, Canada, and Australia, where lenders apply similar debt-to-income limits even when the local terminology differs.

Common Mistakes and Misconceptions

Mistake one: comparing only the principal-and-interest figure. Two homes with the same P and I can have wildly different total payments once property taxes, insurance, PMI, and HOA dues are added. Always compare full PITI, not the headline number.

Mistake two: assuming a fixed-rate payment never changes. The principal and interest is fixed, but the T and I are not. Property tax assessments rise and insurance premiums climb, so your escrow portion grows over time. Many buyers are blindsided by a payment increase in year two even on a fixed-rate loan.

Mistake three: believing extra payments shorten the loan only a little. They do the opposite, because early payments attack a high balance before interest can compound. On that $300,000 loan at 6.5 percent, adding just $200 a month to principal pays the loan off in about 23 years instead of 30 and cuts total interest from roughly $382,600 down to about $279,200, a saving of over $100,000 from a modest extra payment. Confirm with your lender that extra funds are applied to principal, not prepaid toward next month's bill.

Mistake four: thinking PMI cancels itself the moment you hit 20 percent equity from rising home values. The automatic legal termination is tied to your original amortization schedule reaching 78 percent, not to market appreciation. To use a higher home value, you generally must request cancellation and often pay for an appraisal.

Mistake five: stretching to the maximum the 28/36 rule allows. That rule is a ceiling, not a target. It ignores retirement saving, childcare, medical costs, and emergencies. Many financially comfortable households deliberately stay well under 28 percent.

Quick Answers to the Questions Buyers Ask Most

How is a mortgage payment calculated? The principal-and-interest portion comes from the standard amortization formula using your loan amount, your monthly interest rate, and your number of payments. Then you add monthly property tax, homeowners insurance, any PMI, and any HOA dues to get the full payment, known as PITI.

What is PITI? It stands for Principal, Interest, Taxes, and Insurance, the four core components of a monthly mortgage payment. In everyday use people also fold in PMI and HOA dues when those apply, so PITI is shorthand for your true all-in monthly housing cost.

What is PMI and when does it stop? PMI is private mortgage insurance, charged when your down payment is under 20 percent, and it protects the lender. You can request cancellation at 80 percent loan-to-value, and by US law it must terminate automatically once your scheduled balance reaches 78 percent of the original home value, as long as your payments are current.

Is a 15-year or 30-year mortgage better? Neither is universally better. A 15-year loan has higher monthly payments but saves you well over $200,000 in interest on a typical $300,000 loan, while a 30-year loan keeps monthly costs low and preserves flexibility. Choose based on whether you value cash-flow breathing room or long-term savings more.

Does paying extra principal really help? Yes, dramatically, especially early in the loan when your balance and interest charges are highest. Even a small recurring extra payment can shave years off the term and save tens of thousands in interest, because every extra dollar of principal stops accruing interest for the rest of the loan.

Run Your Own Numbers

Understanding the formula is one thing; seeing it applied to your exact situation is another. Small changes in rate, term, down payment, or property tax can swing your monthly payment by hundreds of dollars, and the only way to see the real picture is to plug in your own figures.

Use our free Mortgage Calculator at https://stringtoolsapp.com/mortgage-calculator to do exactly that. Enter your home price, down payment, interest rate, and term, and it computes your principal and interest, layers in property tax, homeowners insurance, PMI, and HOA dues for a true PITI total, and produces a full amortization schedule so you can watch the interest-to-principal split shift month by month. Try a 15-year against a 30-year, test the effect of an extra $200 a month toward principal, and check your payment against the 28/36 affordability rule before you ever talk to a lender.

A quick but important disclaimer: every figure in this guide is an estimate for educational purposes. Actual loan terms, insurance costs, tax rates, and PMI rules vary by lender, location, and your personal financial profile, and government-backed loans follow different rules than conventional ones. Always confirm the specifics with a licensed lender or a qualified financial professional before making a decision. Run the numbers first, ask questions second, and sign last.